Microeconomics Chapter 1

Scarcity

All resources are limited, some more than other - have to manage these while fulfilling as many economic wants

Examples:

Having to add a minimal amount of armor to fighter jets so they don’t get shot down.

Increasing minimum wage pays some people more, but also forces businesses to hire less people

Economists must see possible consequences - can’t just analyze what is there, have to predict what is not

Scarcity - limited resources, unlimited economic wants

Capital goods vs. consumer goods

Capital goods: government spending, more money spent on capital goods -→ future economic growth

Consumer goods: providing resources to people - helpful to people in short term, but doesn’t encourage long term growth

Resources: Land, Labor, Capital, and Entrepreneurial ability

Economics focuses on how to deal with scarcity - macroeconomics deals with entire economy, micro deals with specific markets

Cannot do economic experiments, way too many variables in the environment; Make assumptions to explain some things

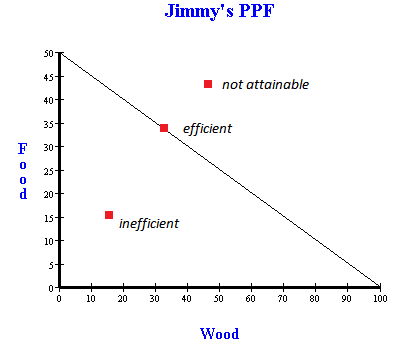

Production Possibilities Curve

PPC - Used to see the maximum amount of products that can be created with scarce resources

Anything on the line is and efficient use of resources - Inside is inefficient, outside is not attainable

Model makes assumptions as mentioned before - full employment, fixed resources, fixed technology

Opportunity Cost - Basically the cost of choosing one option over another

Example: If you make 10 dollars in a day and decide to go on vacation for 4 days, the opportunity cost is 40 dollars

Example: Opportunity cost per unit of wood is 5 units of food/20 units of wood: 1/4 unit of food per unit of wood

Minimal opportunity cost = maximum utility

Opportunity cost per unit = give up/get

Opportunity cost of food = reciprocal of opportunity cost of wood: 4 units of wood per unit of food

Marginal Analysis - Analyzing benefits vs. costs of economic decisions

MR = MC (Marginal Revenue >= Marginal Cost; Otherwise, Opportunity cost is too high)

Graph shows constant opportunity cost - As you make more wood, you are losing a fixed amount of food, and vice versa

This graph shows increasing opportunity cost: Basically, as you give up more resources for making one thing to make another thing, those resources are less suited to make the new thing, so the opportunity cost is higher

Economic Growth = growing the curve so it reaches farther out;

More resources, or improved resources

Better Education

Better technology

Also possible with international trade

Some pitfalls in Economics:

Bias - “First rule of economics → scarcity, first rule of politics → forget rule one of economics.”