Total cost

Total=fixed costs + variable cost

Profits

profit=total revenue - total costs

Total variable costs

Variable cost per unit x Nr of units sold

Sales revenue

Sales revenue = selling price per unit x Nr of units sold

Market capitalisation

Nr of shares issues x current share price

E.V.

EV= pay-off x probability

Net Gain

NG= EV- initial cost of decision

Market size volume

Volume= quantity of goods & services produced in a market in a given time period

Market size value

Total market sales revenue over a given period of time within a market

Sales volume

Quantity of goods and services sold by a business over a period of time

Market growth %

MG= new size-old size / old size x 100

Market share %

Sales of brand/business / total market sales

Added value

Sales revenue - cost of bought /materials

Labour productivity

LP= output per time period / Nr of employees

Unit costs

Total production cost / Nr of units

Capacity utilisation

Actual output / maximum possible output x 100

RoI %

ROI = return on investment / cost of investment x 100

Gross profit

GP = sales revenue - cost of sales

Operating profit

OP = sales revenue - cost of sales - operating expenses

Profit for the year

PfY= operating profit + other profit - net finance costs - tax

Variance

Difference between actual and budgeted figure

Contribution per unit

CpU = selling price - variable costs per unit, It focuses on the returns (contribution) a business makes from each unit of product sold and whether that return is enough to allow the business to make money overall after taking account of its fixed costs.

Total contributions

TC = contribution per unit x units sold

TC = total revenue - total variable costs

Break even output

BE output = fixed costs / contributions per units

Break even chart

When total revenue = total cost

Margin of safety

MoS = actual level of output- break even level

Gross profit margin

GpM = gross profit / sales revenue x 100

Any margin calc

Margin % = ANY profit / sales revenue x 100

Labour turnover %

= Nr of staff leaving / average Nr staff employed x 100

Retention rate %

Nr of staff staying / average Nr staff employed x 100

Employee costs as % of turnover

Employee costs / sales revenue x 100

Labour cost per unit

Labour costs / units of output

ROCE

ROCE = operating profit / (total equity + non-current liabilities) x 100

Current ratio

Current assets / current liabilities, Current ratio is a financial metric used to evaluate a company's ability to pay its short-term liabilities with its short-term assets.

Gearing %

Gearing = non-current liabilities/ ( total equity + non current liabilities) x100, measures how much a company's operations are funded by a form of equity versus debt.

Payable days (creditors)

Payables / cost of sales x 365

Receivable days (debtors)

Receivables / sales revenue x 365

Inventory turnover

IT = cost of goods sold / average inventory held

ARR %

ARR = (net return from project / nr of years) / initial cost

SCORE

Application,

S = size & sector

C = costs, customers, & competition

O = ownership & objectives

R = resources

E = external environment

HWH

Analysis,

H = how X could lead to this initial effect Y

W = why initial effect Y leads to Z

H = how Z impacts the business

AJIM

Evaluation,

A = answer the question

J = justify judgment

I = it depends on

M = most important reason leading to judgement

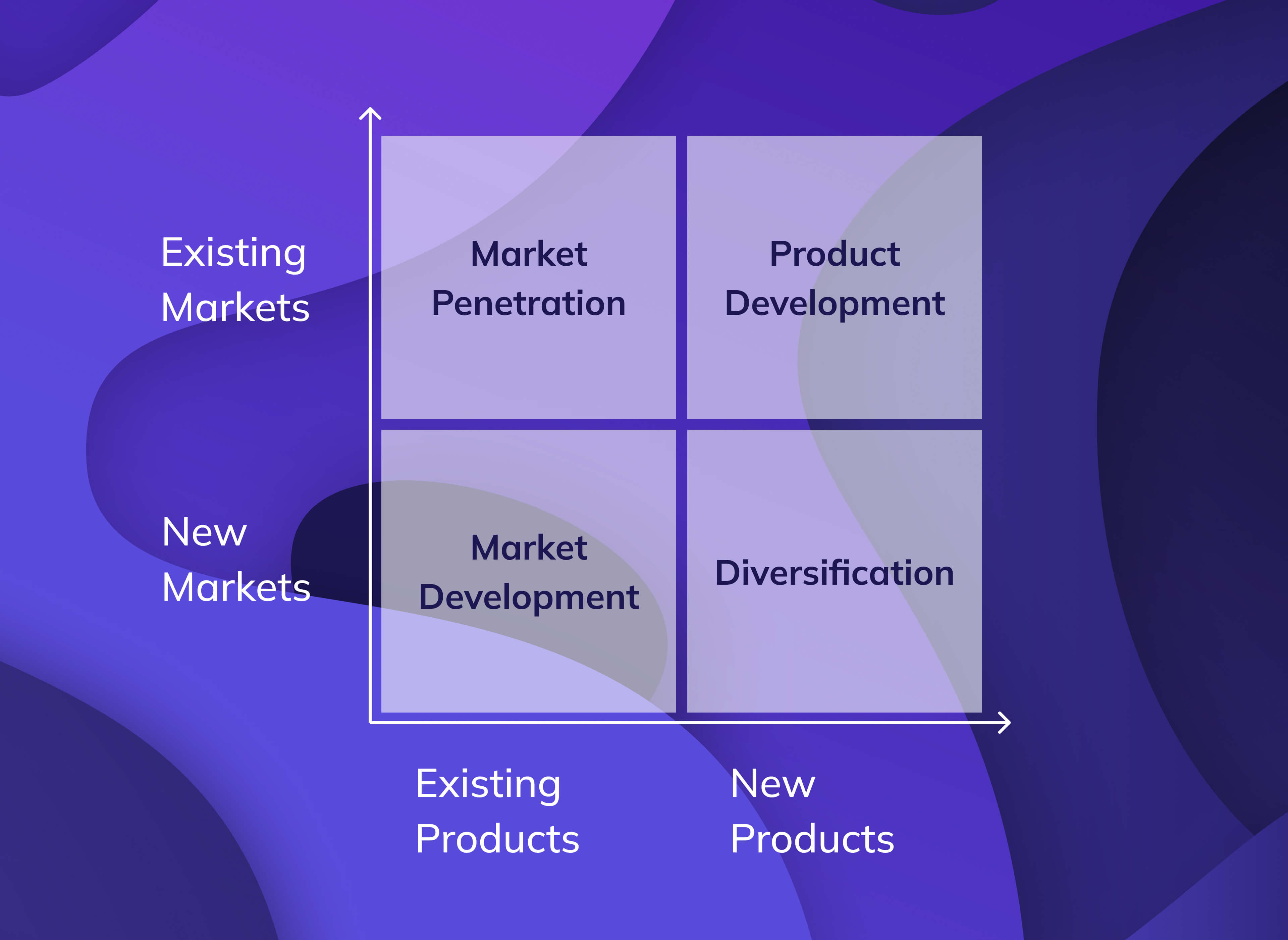

Ansoff’s matrix

4 marketing strategies depending on the relative risk of the respective market and product

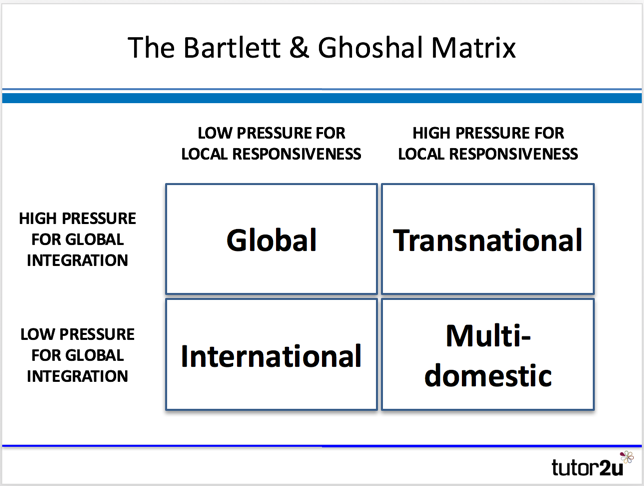

Bartlett & Ghoshal model

Options to manage international operations based on local responsiveness & global integration

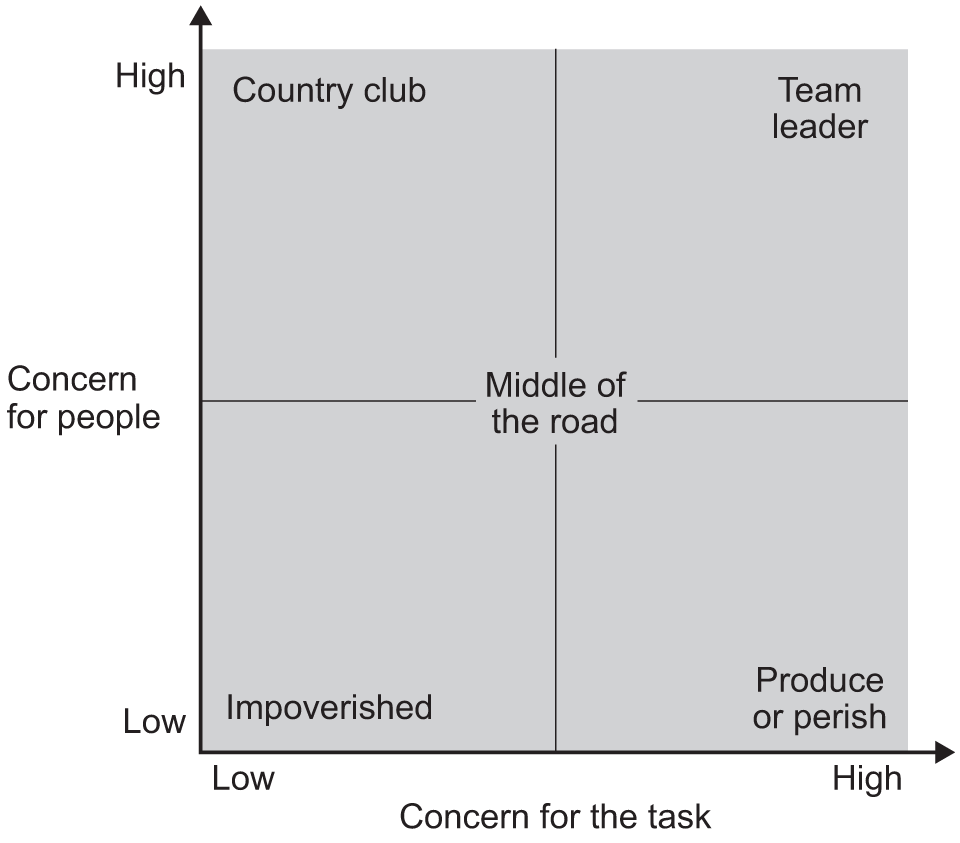

Blake - Mouton grid

5 management styles based on concern for task & people

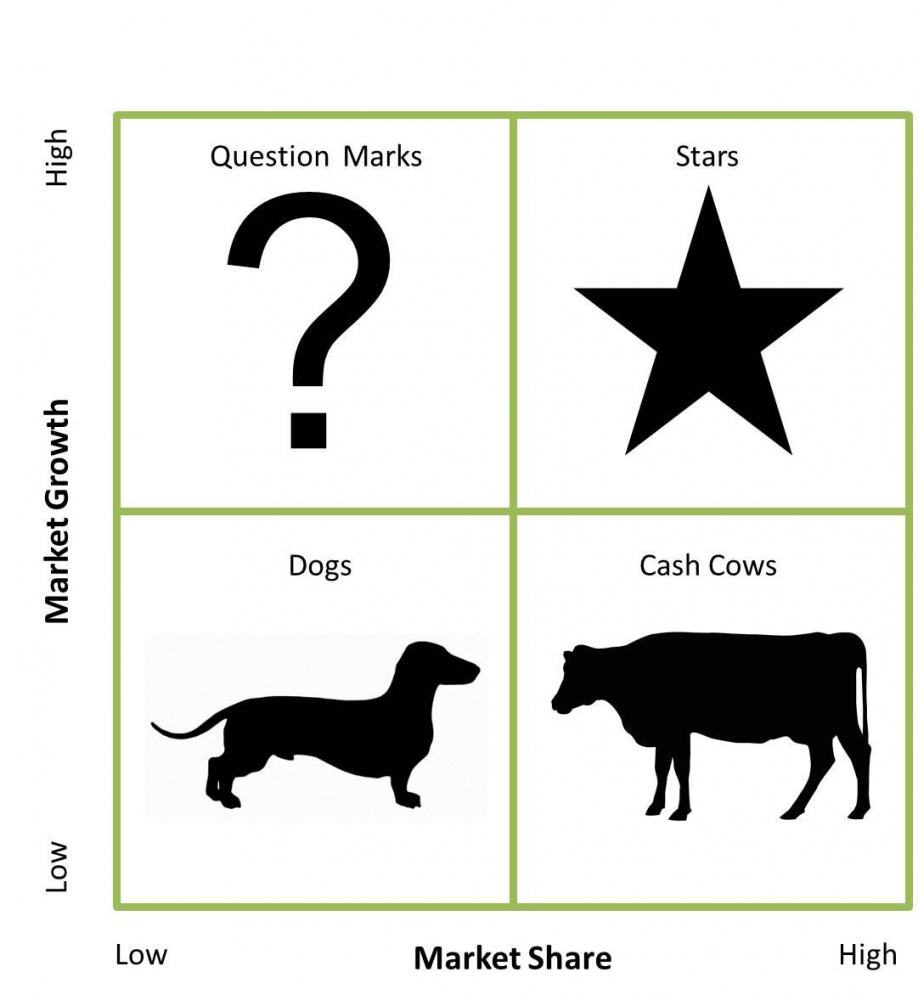

Bostons’ matrix

Product positioning based on relative market growth and market share

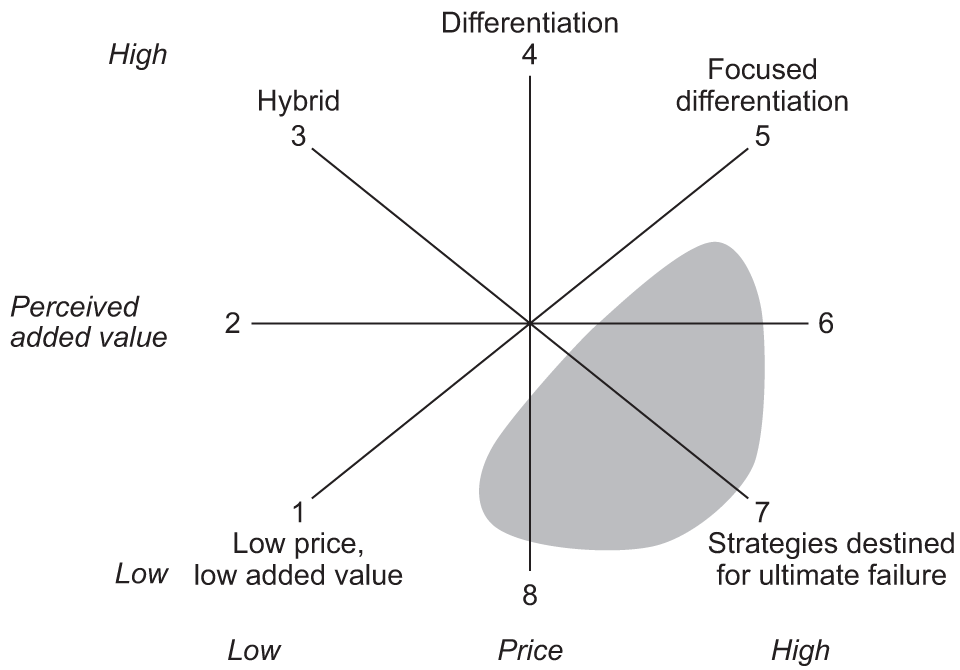

Bowman’s strategic clock

8 product positions based on price an perceived value

6,7,8 = strategic failure (risky high margins, monopoly pricing, loss of market share)

3,4,5 = best strategy as profit & perceived value are highest (hybrid, differentiation, focused differentiation)

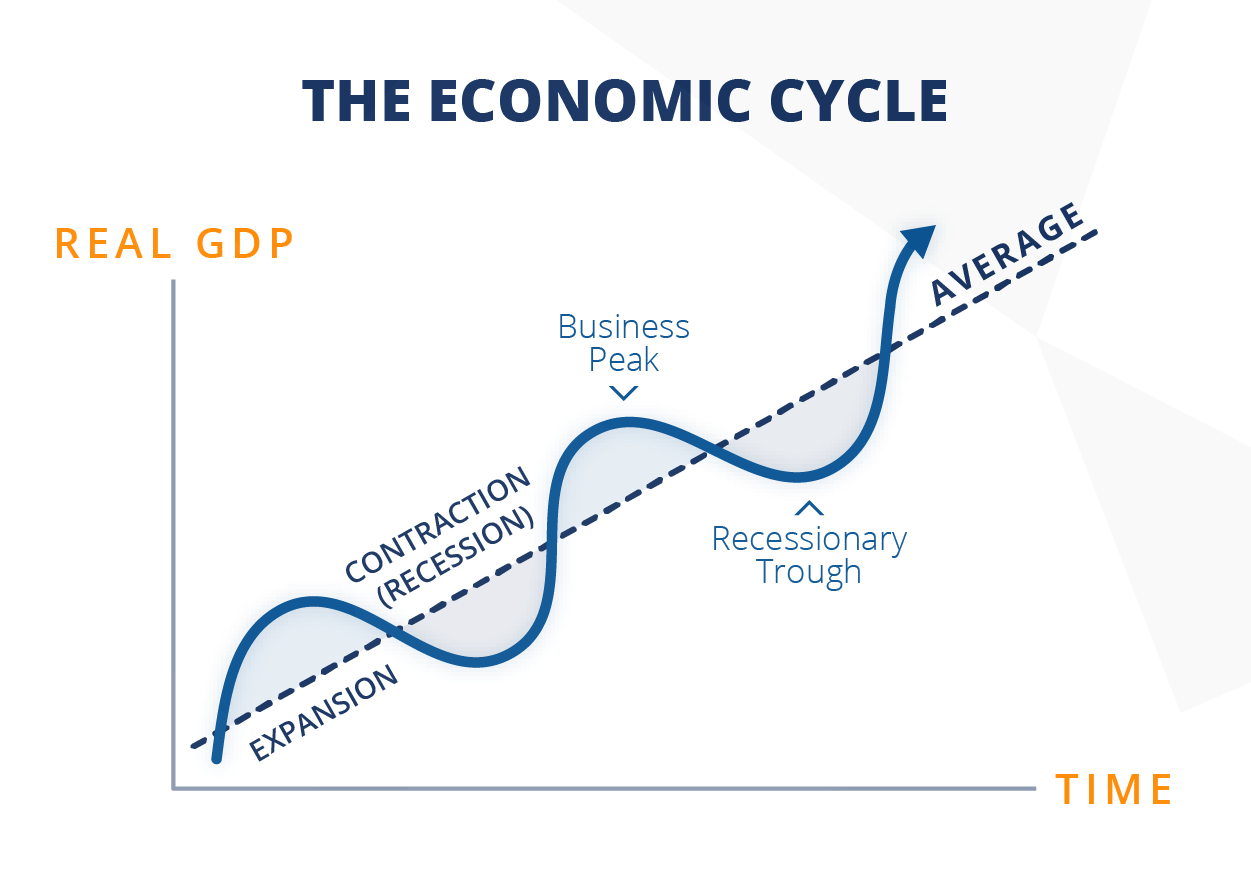

Business cycle

Phases of expansion and contraction of the economy

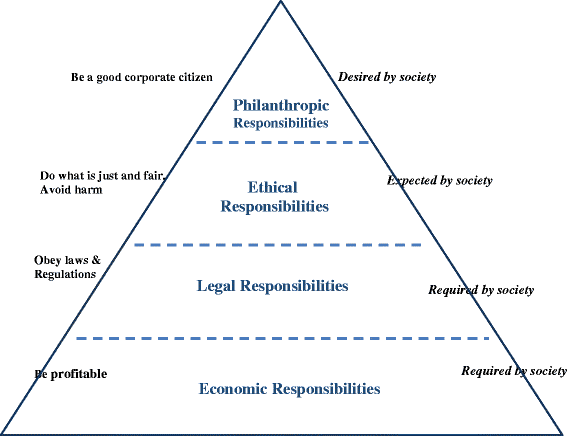

Carrol’s CSR pyramid

Economic - Legal - Ethical - Philanthropic

Elkintons triple bottom line

Profit, People, Planet

The model highlights that business performance may be measured in a number of ways: in relation to its finances, its environmental impact and how socially responsible it is in relation to employees.

Elkington argued that only a company that was measuring performance in all three areas was measuring the full costs of its activities. The significance of this is that if you measure all these areas employees are likely to pay attention to them and change their behavior accordingly (rather than just focusing on profit).

The experience curve

Unit costs fall as cumulative production increases

more experience = less mistake = lower costs

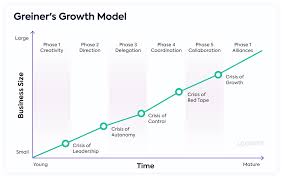

Greiner’s growth model

6 phases & 5 crisis

creativity & leadership

Direction & autonomy

Delegation & control

Coordination & red tape

Collaboration & growth

Alliances

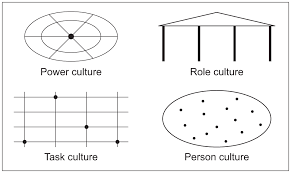

Handy’s cultural model

4 types of cultures

power based (few have power, few rules, intuition based)

Role based (role derived power, little scope, bureaucracy)

Task based (Teams for particular projects, Power derives from expertise, Matrix organisation)

Person based (ability based power, person before business, very similar training/expertise)

Hofstede’s national cultures

6 ways culture varies in different countries

individual vs collective

Power distance

Short vs long-termism

Masculinity vs femininity

Uncertainty avoidance

Indulgence vs restraint

Kaplan & Nortons balanced scorecard

4 perspectives that give management a broader view of business performance

vision & strategy

Financial

Internal processes

Organisational capacity

Customer

Kotter & Schlesinger

4 causes and 6 solutions to resistance to change

Causes:

Self-interest

Disagree with the situation/method

Low tolerance for change

Misinformation/misunderstanding

Solutions:

education & communication

Participation & involvement

Support

Manipulation & co-option

Negotiations & bargaining

Explicit & implicit coercion

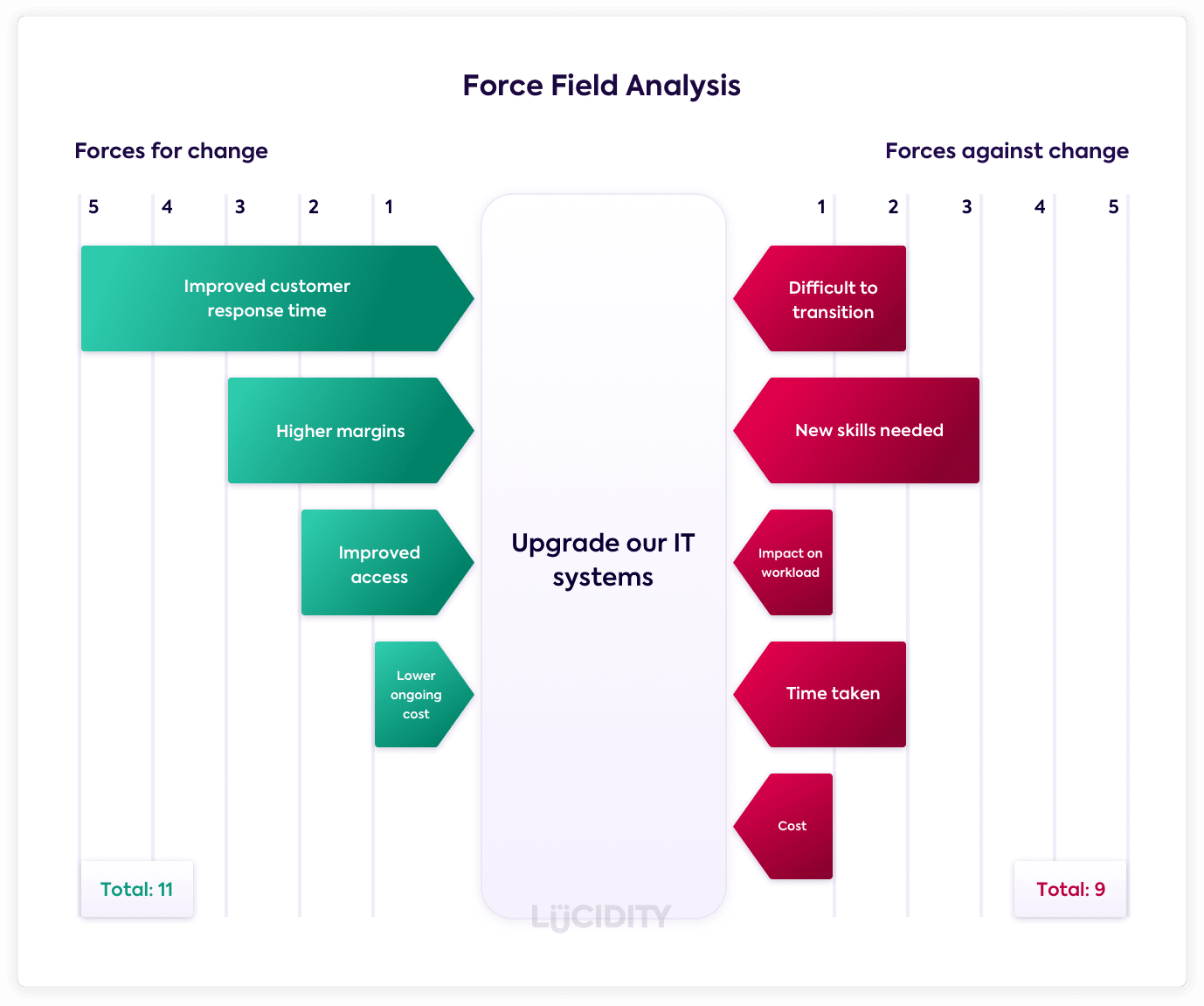

Lewin’s field force analysis

Driving forces vs restraining forces to determine/calculate wether change is viable

simplistic

Doesn’t quantify each force

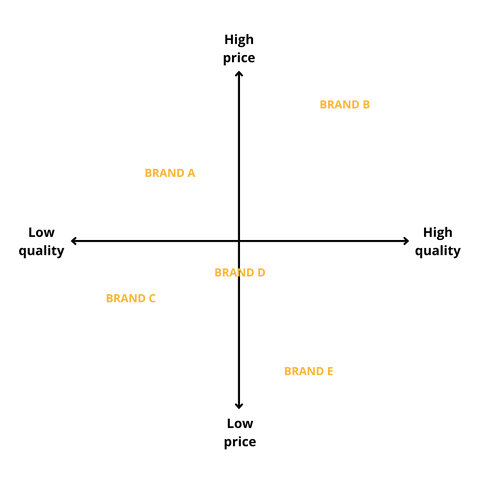

Market mapping

Mapping to determine competitive position regarding price and quality

Utilises a x & y axis, where the x-axis = quality, and the y-axis = price

Extended marketing mix (7 P’s)

Price

Promotion

Place

Physical environment

People

Process

Product

Masllow’s hierarchy of needs

Physiological - safety - social - esteem - self actualisation

Pestle analysis

External influences that affect strategy

Political

Economic

Social

Technological

Legal

Ethical/Environmental

Porters’ 5 forces

5 forces which analyse the nature of the competitive environment

rivalrous intensity

Threat of substitutes

Threat of new entrants

Bargaining power of suppliers

Bargaining power of customers

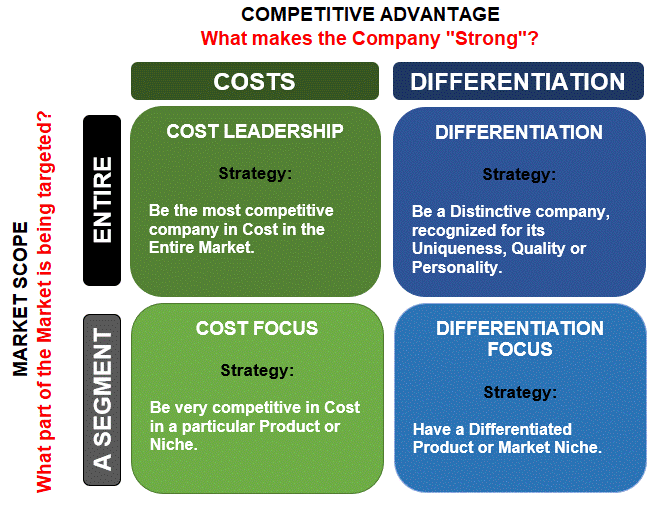

Porters’ generic strategies

Generic strategies to utilise/create a competitive advantage based upon the nature of this advantage (cost or differentiation) and the nature of the market (broad or narrow)

cost leadership (cost & broad)

Cost focus (cost & narrow)

Differentiation leadership (differentiation & broad)

Differentiation focus (differentiation & narrow)

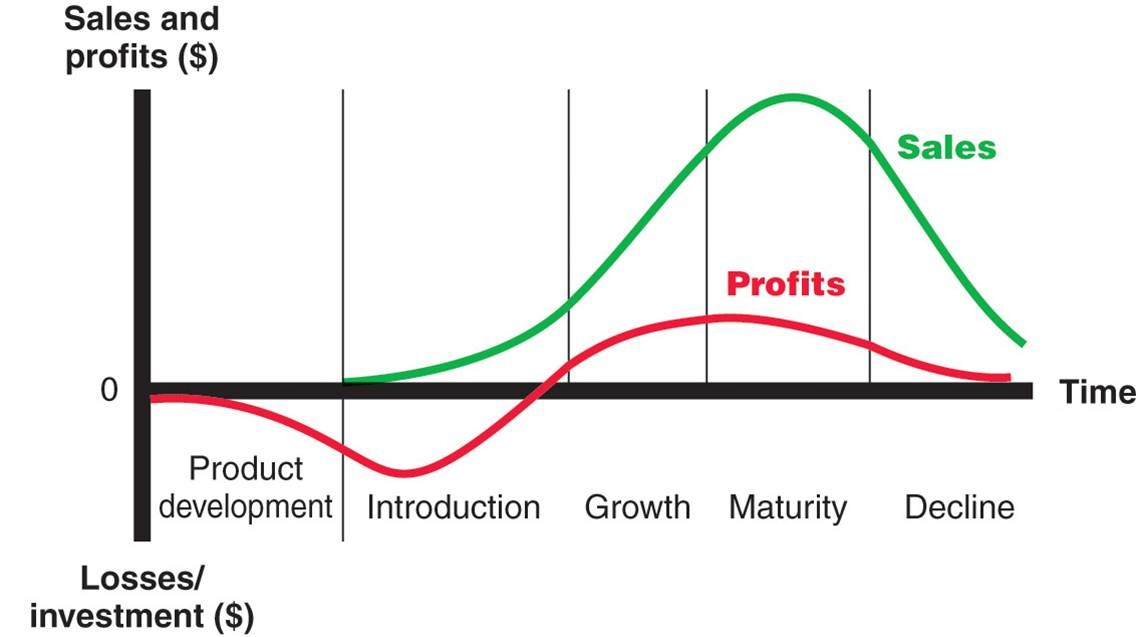

Product life cycle

research & development

Introduction

Growth

Maturity

Decline/extension

Scientific decision making process

set objectives - gather data - analyse data - select - implement - review

STP (marketing)

3 marketing strategy choices

Segmentation:

demographic, geographic, income, behaviour

Targeting:

mass (mass), segmented (differentiated), concentrated (niche)

Positioning:

place a product occupies in the consumers mind relative to competing products

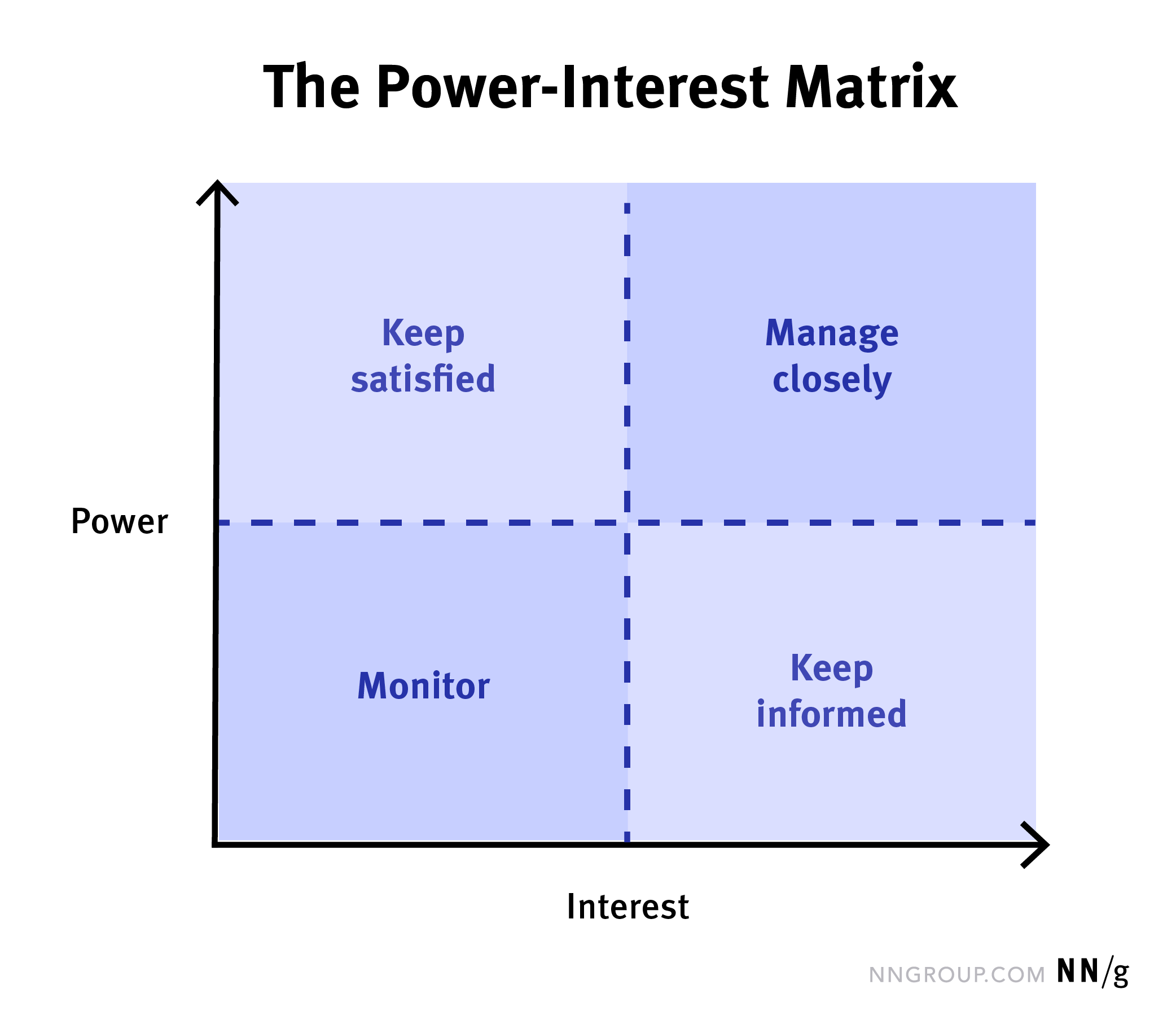

Stakeholder mapping

Stakeholder approach based upon stakeholder interest & power

low & low = monitor

Low interest & high power = keep satisfied

High interest & low power = keep informed

High & high = manage closely

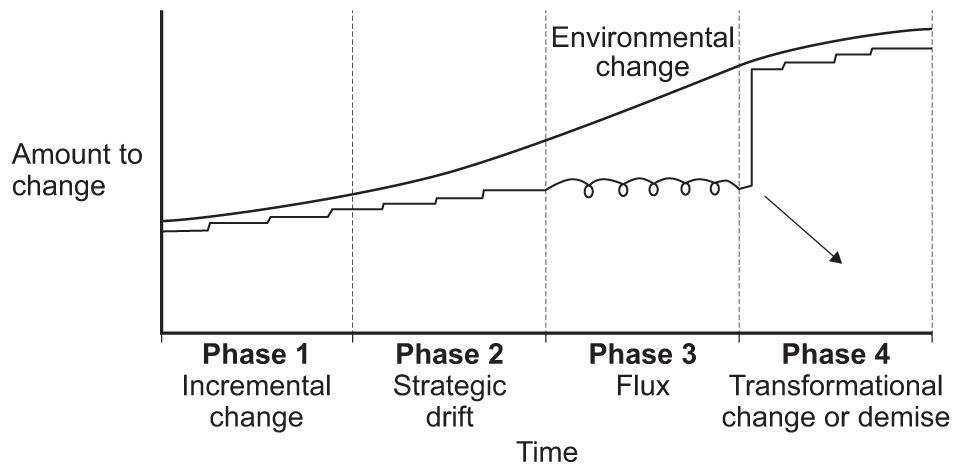

Strategic drift

When strategy diverts from the change that is needed to adapt to its external environment

incremental change

Strategic drift

Flux

Step transformation or death

Swot analysis

Analysis of internal & external pressures affecting a business

Strenght

Weaknesses

Opportunities

Threats

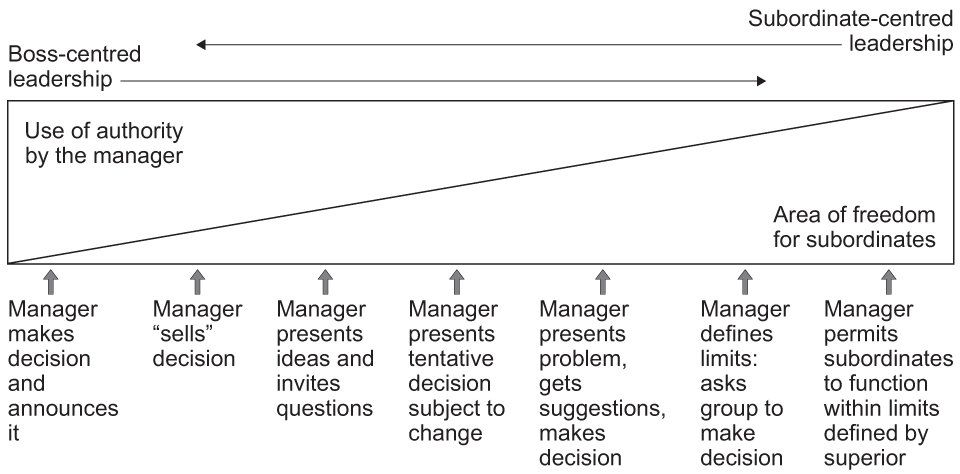

Tannenbaum Schmidt continuum

Managerial positioning based upon how much freedom they allow subordinates (from autocratic to democratic) (from authoritarian to laissez-faire)

Tell - Sell - Consult - Join

Variance formula

Actual - Budget

Income statement

Statement recording all inflows & outflows of cash, revenue (+other incomes) and expenditures

Balance sheet

Statement recording all assists and liabilities a firm has