Chapter 10: Pure Monopoly

Pure monopoly - Single firm is sole producer of product w/ no close substitutes

Single seller

No close substitutes

Price maker - Can change price of product

Blocked entry - No potential competitors can enter industry

Non-price competition - Monopolists that have standardized products engage mainly in public relations advertising

Ex. Government-owned public utilities, professional sports teams, etc.

Barriers to entry - Factors that prohibit firms from entering industry

Block potential competition

Exists in market structures w/ monopolistic behavior

Economies of scale

Produce more → Gets cheaper to produce

Caused by modern technology

Entry barrier that protects from competition

Legal barriers to entry

Patent - Exclusive right to use/allow another to use invention

Protects from rivals

Monopoly for life of patent

Funds R&D

License

Limits entry into industry/occupation

Ownership of resources

Owns/controls specific resource → Can prohibit entry of other firms

Pricing

Slashing prices + increasing advertising → Rivals cannot succeed

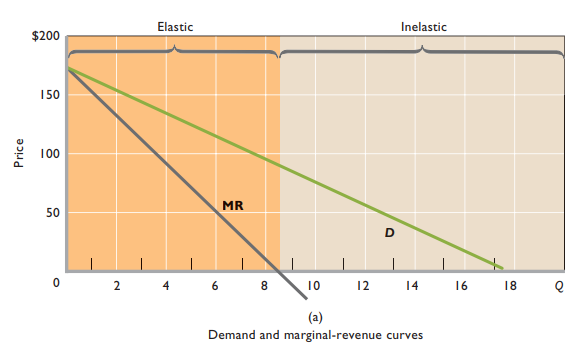

Monopoly demand

Monopolist’s demand curve = Market demand curve

Down-sloping demand curve

Marginal revenue less than price

Each additional unit of output sold increases total revenue by an amount equal to its own price less the sum of the price cuts that apply to all prior units of output

Total revenue increases at diminishing rate

MR curve below demand curve

Price maker

Change market supply → Influence product price

Sets prices in elastic region of demand

Always avoids inelastic portion of demand curve

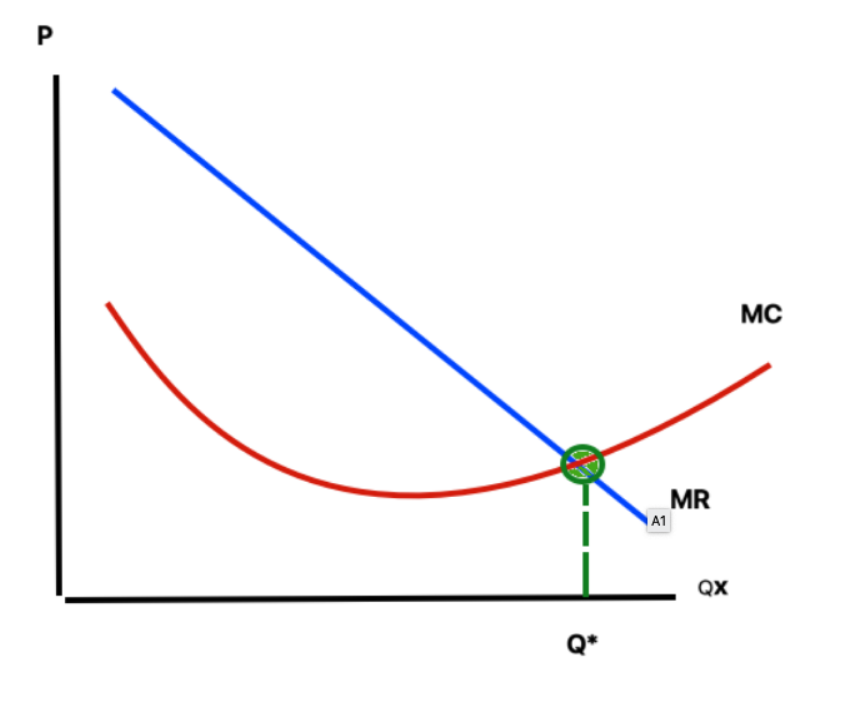

MR = MC

Vertical line from quantity where MR = MC to demand curve = Price that monopolist charges

No supply curve

Seeks max total profit, not max prices

Seeks max total profit, not max unit profit

No guaranteed profit

Not immune to changes in consumer tastes or reduced product demand

Price greater than average variable cost → Continues to produce instead of shutting down

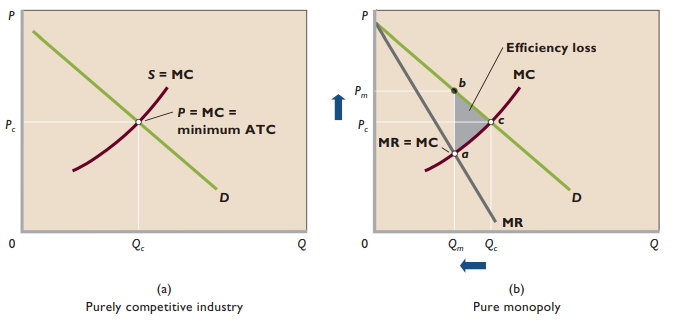

Economic effects

Neither productive nor allocative efficiency

Underallocation of resources

Sum of consumer surplus + producer surplus less than max

Income transfer

Owners of monopolies benefit at cost of consumers

Increases income inequality

Cost complications

Sometimes only natural monopoly can achieve lowest long run average total cost

Simultaneous consumption - Product’s ability to satisfy large # of consumers at same time

Network effects - Value of product to each user increases as total number of users increases

X-inefficiency - Firm produces output at higher cost than necessary to produce

Caused by lack of competitive pressure

Rent-seeking behavior - Activity designed to transfer income/wealth to a firm/resource supplier at someone else’s expense

Pure monopolists are not technologically progressive

Assessment + policy options

Monopolies are problems

New technologies can destroy monopolies

New products circumvent patent advantages

Possible actions

Gov’t files charges under antitrust laws

Gov’t regulates monopoly’s prices + operations

Society ignores it

Price discrimination - Selling a specific product at more than one price when the price differences are not justified by cost differences

Conditions

Monopoly power

Market segregation

No resale

Enhances profit

Regulated monopoly

Multiple firms would incur higher average total costs than 1 firm

Socially optimal price - Allocative efficiency; P = MC

Fair-return price - Permits fair return to firm owners; P = ATC