Economics 1: Basic concepts of economics

Types of Sciences:

Natural Sciences: These encompass laws that are universally accepted and can be empirically tested under controlled laboratory conditions. These sciences are often referred to as exact sciences.

Examples: Mathematics, Physics, Chemistry.

Social Sciences: Often labeled as abstract or behavioral sciences, these fields focus on understanding various aspects of human behavior. They deal with human behavior that cannot be empirically tested in a laboratory. Consequently, the laws of social sciences are not universal, but rather statements of general human tendencies.

Examples: Psychology (mental aspects of human behavior), Sociology (social aspects of human behavior in a societal context).

What is economics?

Economics is considered a social science.

The term 'Economics' has its origins in the Greek word 'Oikonomia,' which translates to the management of a household.

Paul Samuelson famously referred to Economics as the 'Queen of Social Sciences.'

Economics primarily focuses on the economic dimensions of human behavior, specifically how individuals address unlimited wants with limited resources.

Understanding the Nature of Economics:

Economics examines the economic facets of human existence.

It revolves around the core concept of resource allocation and the choices people make to meet their insatiable desires using finite resources.

Kautilya's Views on Economics:

Kautilya, an ancient Indian philosopher and economist, shared profound insights on economics in his work "Arthashastra," a treatise on the science of acquiring and managing wealth, which aligns with what we now call political economy.

Key Elements of Kautilya's Economic Views:

The crucial role of the state or government:

Kautilya emphasized the state's significance in economic matters. He believed that a strong state actively participating in economic activities was crucial for stability.Wealth Creation for Welfare:

Kautilya advocated wealth creation as the primary goal of the state to ensure citizens' welfare and happiness.Efficient Administration:

He recognized the need for an efficient administrative system to implement economic policies effectively.Compilation into Arthashastra:

Kautilya's ideas were consolidated into the Arthashastra. It remains a valuable source for understanding ancient Indian economic philosophy and governance.

Summary: Kautilya's economic philosophy underscores the state's role in wealth creation and the importance of efficient administration in fostering prosperity.

(1) Adam Smith's Wealth-Oriented Definition of Economics:

Adam Smith, a classical economist often referred to as the "Father of Economics," provided a wealth-oriented definition of Economics.. Smith is renowned for his 1776 masterpiece, "An Inquiry into the Nature and Causes of the Wealth of Nations," in which he laid the foundation for his economic theories.

Definition of Economics: According to Adam Smith, Economics is "a science of wealth." This definition encapsulates his perspective on the subject.

Key Points:

Laissez-Faire:

Smith advocated the principle of "Laissez-faire," which promotes minimal government intervention in economic activities. He believed that market forces should operate without excessive regulation.Capital and Wealth Accumulation:

Central to Smith's view was the idea that the pursuit of wealth through individual effort and entrepreneurship was a driving force of economic growth.Nature's Law in Economic Affairs:

Smith argued that there are natural laws governing economic activities. These laws are driven by self-interest and competition among individuals.Division of Labour:

Smith highlighted the concept of the division of labor as a critical aspect of economic growth. When work is divided and specialized, it leads to increased productivity and efficiency.

Summary: Adam Smith's ideas, particularly his support for minimal government intervention, have had a profound influence on classical economics and continue to shape economic thought and policy today.

(2) Prof. Alfred Marshall's Welfare-Oriented Definition of Economics:

Economics, as presented by neo-classical economist Prof. Alfred Marshall in his 1890 book "Principles of Economics."

Definition of economics: Economics is a study of mankind in the ordinary business of life. It examines that part of individual and social action, which is closely connected with the attainment and use of material requisites of well-being.

Key Points:

Study of an Ordinary Man: Marshall's economics focuses on the common individual, emphasizing the study of everyday people and their economic actions.

Economics as a Behavioral Science: It views economics as a behavioral science, exploring how individuals and societies behave in their quest for material well-being.

Study of Material Welfare: The core concern is material well-being and the resources needed to achieve it, emphasizing the importance of understanding how people satisfy their material desires.

Economics Not Just About Wealth: Marshall's definition goes beyond the mere accumulation of wealth; it encompasses the broader context of individual and social well-being.

Summary: Alfred Marshall's definition of economics underscores its role as a social science that analyzes the behavior of ordinary people in their pursuit of material well-being, moving beyond a narrow focus on wealth accumulation.

(3) Lionel Robbins' Scarcity-Oriented Definition of Economics:

Lionel Robbins, in his influential 1932 book "An Essay on the Nature and Significance of Economic Science," introduced the scarcity-oriented definition of economics.

Definition of economics: Economics is a science that studies human behavior as a relationship between ends and scarce means that have alternative uses.

Key Points:

Wants (Ends) are Unlimited: People have endless desires or wants. They always want more and different things to make their lives better or more comfortable.

Means are Comparatively Limited: In contrast to unlimited wants, the resources or means available to fulfill these wants are not unlimited. They are limited; there's only so much to go around.

Wants are Gradable on the Basis of Priority: People prioritize their wants; some things are more important or urgent than others. For example, having food and shelter might be more urgent than buying a luxury item.

Means Have Alternative Uses: Resources (means) can be used in different ways. For instance, money can be used to buy various goods, so people have to decide how to use their limited money wisely.

Summary: Robbins' definition highlights the central concept of scarcity: unlimited human wants or desires versus limited resources, which forces people to make choices and prioritize their needs and wants.

Branches of Economics:

In 1933, Sir Ragnar Frisch introduced the terms microeconomics and macroeconomics, derived from the Greek words 'Mikros' and 'Makros' respectively.

(A) Micro-Economics:

Micro means small.

Microeconomics deals with the behavior of individual variables, such as households, workers, firms, and industries.

It focuses on the behavior of individual economic agents.

Kenneth Boulding's Definition of Micro Economics:

Microeconomics is the study of particular firms, particular households, individual prices, wages, incomes, individual industries, and particular commodities.

Basic Concepts of Micro Economics:

(1) Want:

Want is a challenging concept to define concisely. In common language, it can be seen as a need. However, in economics, a want signifies a sense of 'lack of satisfaction,' driving individuals to fulfill their desires.

Reasons for the Growth of Human Wants:

Desire for an improved standard of living through inventions and innovations.

Population growth.

Characteristics of Wants:

i) Unlimited:

Wants are never-ending. As one is satisfied, another arises, leading to an endless cycle of desires.ii) Recurring in Nature:

Many human wants occur repeatedly, while some may be occasional.iii) Age-Dependent:

Wants and their fulfillment vary with a person's age.iv) Gender-Specific:

Men and women have different preferences and want different goods based on their needs.v) Influenced by Preferences:

Individual habits, tastes, and preferences significantly affect what people want.vi) Seasonal Variations:

Wants change with seasons. For instance, demand for warm jackets rises during winter.vii) Cultural Influence:

Cultural differences impact wants related to food, clothing, and other aspects.Classification of Wants:

i) Economic and Non-economic Wants:

Economic wants involve monetary transactions, requiring payment, e.g., food or medicines. - Non-economic wants can be satisfied without monetary payment, e.g., air or sunshine.ii) Individual Wants and Collective Wants:

Individual wants are those satisfied at an individual level, e.g., a doctor using a stethoscope or a judge wearing a coat. - Collective wants are social wants collectively satisfied, e.g., traveling by train.iii) Necessities, Comforts, and Luxuries:

Necessities are the most fundamental life needs, like food, clothing, shelter, health, and education. - Comforts fulfill wants that make life comfortable, such as washing machines, mixers, or pressure cookers. - Luxuries are wants meant for pleasure and enjoyment, such as AC cars or well-furnished houses.

(2) Goods and Services:

Goods are things that satisfy human wants, and they have a material existence. For example, a chalk used by a teacher is a good.

Services also satisfy human wants, but they don't have a physical form or material existence. An example of a service is the 'teaching' provided by a teacher.

(3) Utility:

Utility is a crucial concept in economics.

It refers to the capacity of a commodity to satisfy human wants, or in simpler terms, it's the commodity's power to fulfill our needs and desires.

The concept of utility helps us understand how valuable a product or service is to people, based on how much it fulfills their wants and needs.

(4) Value:

Value is a core concept in economics, approached through 'value-in-use' and 'value-in-exchange.’

Value-in-Use:

Refers to the worth or usefulness of a commodity for a specific purpose. For example, sunshine's value lies in its role in sustaining life, and it's often considered a "free good."

Value-in-Exchange:

Reflects a commodity's worth expressed in terms of money. Commodities with exchange value command prices and are termed "economic goods" (e.g., TVs and cars).

Water-Diamond Paradox of Values:

Highlights the contrast between value-in-use and value-in-exchange. Water, vital for survival, has low exchange value due to abundance, while diamonds, less essential, have high exchange value due to scarcity.

(5) Wealth:

Wealth is a significant concept in economics, defined as "anything that has market value and can be exchanged for money." To be considered 'wealth.'

Characteristics of wealth:

i) Utility:

A commodity must have the capacity to satisfy human wants, such as furniture or a refrigerator, by being useful.ii) Scarcity:

The commodity must be scarce in supply in relation to its demand to be included in the term 'Wealth.' This applies to all economic goods for which a price is paid.iii) Transferability:

A commodity should be transferable from person to person as well as from place to place. If the good is material or tangible, it can be moved, like a vehicle or jewelry.iv) Externality:

A good can be transferred only if it is external to the human body. Items like bags or chairs can be examples of externally transferable goods.

(6) Personal Income:

Personal income refers to the total earnings received by an individual from all sources. Foe example: wages, salaries, investment income, and any other sources of earnings.

(7) Personal Disposable Income (PDI):

Personal disposable income represents the portion of an individual's income that remains after deducting direct taxes such as income tax and other levies. It is the income that an individual has at their disposal for personal consumption and saving after paying their direct tax obligations.

(8) Economic Activity:

Economic activities encompass various processes that drive an economy and can be categorized into four types: production, distribution, exchange, and consumption.

a) Production:

Production involves the creation of utility or value.

Four factors of production play a key role in production:

i) Land:

In economics, 'land' is a broad term encompassing all-natural resources available on, above, and below the Earth's surface. Examples include minerals below the surface, soil, water, air, sunshine, and wind. Land earns 'rent' in productive activities.

ii) Labour:

Labour represents the human factor of production. It encompasses the physical and mental efforts undertaken during the production process to earn 'wages.' For example, carpenters, accountants, and engineers.

iii) Capital:

Capital is a man-made factor of production, which serves as a means for further production. It earns 'interest' and includes items like machinery, technology, and factory buildings.

iv) Entrepreneur:

The entrepreneur is the organizer, often regarded as the captain of the industry. They are a special category of labor responsible for overseeing and coordinating the production process, earning 'profits.'b) Distribution:

Distribution involves the division of factor rewards among different segments of society. The factors of production claim their rewards—rent, wages, interest, and profit—through the distribution process.

c) Exchange:

Exchange entails the sale and purchase of goods and services, where transactions are typically monetary in nature. It encompasses the interaction and trade between various units in the economy.

d) Consumption:

Consumption is the utilization of goods and services to satisfy human wants. It represents the final stage of economic activity, where individuals and households use the products and services produced in the earlier stages to meet their needs and desires.

(B) Macro-Economics:

Macro-Economics delves into the study of large-scale economic aggregates that encompass the entire economy. These aggregates include total employment, national income, output, investment, savings, consumption, aggregate supply and demand, and the general price level.

Kenneth Boulding's Definition:

Kenneth Boulding describes macroeconomics as the study of economic aggregates, not individual quantities. It focuses on the collective aspects of economics, including national income, general price levels, and national output, rather than isolated components.

Basic Concepts of Macro-Economics:

National Income:

It represents the total income generated within a country. It's the combined monetary value of all final goods and services produced in an economy over the course of a year.

The National Income Committee defines it as "an estimate that measures the volume of commodities and services produced during a given period, without counting duplications."

Saving:

Saving is the portion of one's income set aside to meet future needs by postponing current consumption. In simpler terms, it's the income not currently spent on consumption.

Investment:

Investment refers to the creation of capital assets through the utilization of savings. This includes the acquisition of items like machinery and equipment, contributing to economic growth.

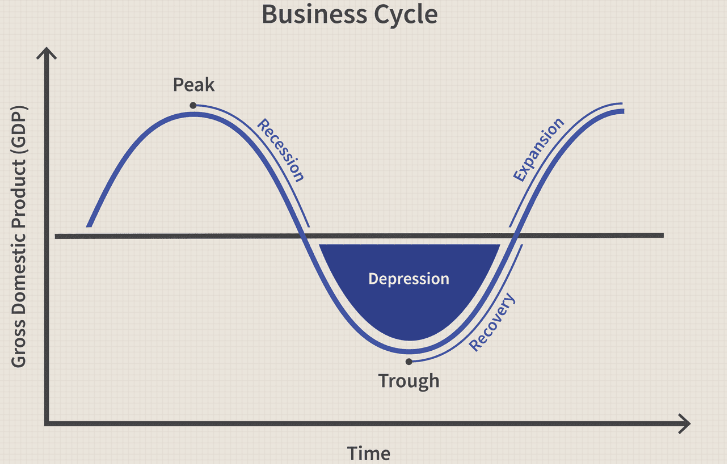

Trade Cycles:

Trade cycles represent fluctuations in economic activity, encompassing both upswings and downturns.

Inflation denotes a continuous increase in the general price level, impacting the purchasing power of money.

Depression refers to a persistent decline in overall prices and a reduction in economic activity.

Economic Growth:

Economic growth has a quantitative aspect. It signifies an increase in a nation's real national income over an extended period.

Economic Development:

Economic development, on the other hand, is a broader concept with qualitative dimensions. It implies not just economic growth but also progressive changes, such as education and health.

Important Questions:

Economic Development vs. Economic Growth

Explain the difference between microeconomics and macroeconomics.

How does economics relate to the field of social sciences, and what is its primary focus?

Discuss the concept of scarcity as defined by Lionel Robbins. How does scarcity drive economic decision-making?

What is the relationship between personal income and personal disposable income (PDI)?

Describe the four economic activities: production, distribution, exchange, and consumption.

Classical vs Neo-Classical economics.