main users difference of cash and profit income statement main financial statements statement of financial position

main users of company accounts

managers, employees, government, competitors, suppliers, customers, local community, shareholders

why managers use company accounts

use information to record financial activities, plan actions, control use of resources and evaluate effectiveness of actions

why employees use company accounts

assess the security of a job, assess ability for fair wages

why do the government use company accounts

check the business meets legal requirements and if they have paid the right level of tax

why do competitors use company accounts

to compare and benchmark performances

why suppliers use company accounts

to help decide if they should agree to supply, and to identify the sort of payment terms offered to other suppliers

why would customers use company accounts

to look for guarantees and if after sales servicing is secure

why do the local community use company accounts

because employment, wealth, housing and road plans depend on the financial state

why do shareholders look at company accounts

to compare financial benefits of their investments

what is cash

the amount of actual money a business has at its disposal

what is profit

the money a business has made after accounting for all expenses

reasons for the difference between cash and profit

receive cash at the beginning of trading year from sales made in the previous year (increase in cash)

owner introduces more cash

purchases of fixed assets reduce cash balance

sales of fixed assets increase cash balance

income statement

summarises income and expenses and details the profits and loses made by the business

uses of an income statement

measures success of the business compared to previous years or other businesses

assesses actual performance of business with expectations

helps obtain loans or finances from banks or lenders

helps plan ahead

advantages of income statement

sees overall profit

shows earnings per share for shareholders

other stakeholders use it to compare

helps control costs

measures growth

disadvantages of income statements

other financial data - cash flow

other business data - social and environmental impact

record of past performance: not always indicator of present or future

trends - 1yrs figure not indicate growth or decline, more periods needed

manipulated accounts to look better

level of detail in the account

profit quality

low profit quality if 1 year is higher than expected but not retains in other years

profit utilisation

the way profit is used after tax e.g. paid out as dividends or retain profit for future use

statement of financial position

summarises the assets, liabilities and capital of a business at a particular date

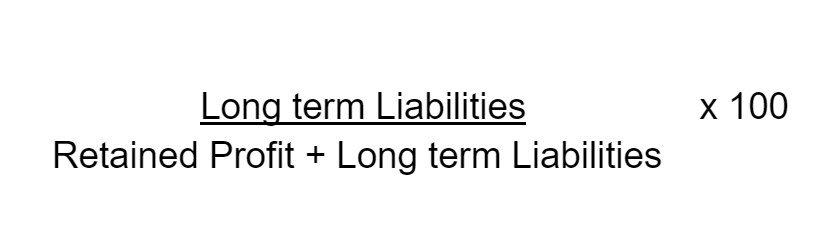

3 key parts to pick out of a statement of financial position

Non Current Assets (business can fall back on this by selling it)

Gearing %: Image

Working capital= Current Assets- Current Liabilities

Evaluation of financial statements (advantages)

Enables management to summarise the financial position of the business at end of accounting period + useful for stakeholders

Income statement: determines profitability and can compare with previous accounting periods or budgets

Statement of FP: helps review FP an provide guidance in effective working capital management

Enables decision to be taken

Owners/Shareholders access to more detailed financial info + enables shareholders to evaluate the management team operating on their behalf

Governments verify the companies liabilities to various forms of taxation and duties

Supplier inspect financial position and make decisions on credit worthiness of company

Evaluation of financial statements (disadvantages)

info may be out of date so no reflect on economic reality

difficult to fully understand content of financial statements and its impossible for external shareholders to gain full understanding

concentrate of quantitative issues effecting the business so limited

difficult for users to compose financial performance with other companies

subject to public scrutiny