Chapter 17: Public Choice Theory and the Economics of Taxation

Public choice theory - Economic analysis of government decision making, politics, and elections

Revealing preferences through majority voting

Decisions about regulation of businesses, income distribution, etc.

Made through majority voting

Vote for officials who represent collective wishes

Inefficient voting outcomes

Inefficient “no” vote → Too little of public good produced

Inefficient “yes” vote → Too much of public good produced

Majority voting cannot incorporate strengths of each person’s preferences

Interest groups - People who share strong preferences for a public good may band together into interest groups and use advertisements, mailings, and direct persuasion to convince others of the merits of that public good

Logrolling - Trading of votes to secure favorable outcomes

“Vote for my special local project and I will vote for yours”

Paradox of voting - A situation in which society may not be able to rank its preferences consistently through paired-choice majority voting

Under some circumstances majority voting fails to make consistent choices that reflect the community’s underlying preferences

Median-voter model - Under majority rule and consistent voting preferences, the median voter will in a sense determine the outcomes of elections

Median voter is person holding middle position

Political candidates appeal to median voter to get nomination

Info about people’s preferences is imperfect → Politicians can misjudge true median position

Government failure - Inefficiency due to certain characteristics of the public sector

Special-interest effect - Any outcome of the political process whereby a small number of people obtain a government program or policy that gives them large gains at the expense of a much greater number of persons who individually suffer small losses

Pork barrel politics - Securing gov’t project that yields benefits mainly to a single district/political representative

Earmarks - Narrow, specifically designated authorizations of expenditure

Logrolling - “Vote for my special local project and I will vote for yours”

Rent seeking - Appeal to government for special benefits at taxpayers’ or someone else’s expense

Politicians favor programs w/ immediate benefits + reject programs w/ very high long-term benefits

The citizen as a voter is confronted with, say, only two or three candidates for an office, each representing a different “bundle” of programs (public goods and services). None of these bundles of public goods is likely to fit exactly the preferences of any particular voter. Yet the voter must choose one of them.

Bureaucracy + inefficiency

Gov’t agencies + managers have no incentive to be efficient

Gov’t bureaucrats justify continued employment by creating + pretending to solve problems

Imperfect institutions

Is an activity performed w/ greater success in private or public sector?

Apportioning the tax burden

Benefits-received principle - Households and businesses should purchase the goods and services of government in the same way they buy other commodities

Those who benefit most from government-supplied goods or services should pay the taxes necessary to finance them

Cannot be applied to income redistribution programs

Ability-to-pay principle - Tax burden should be apportioned according to taxpayers’ income and wealth

Types of taxes

Progressive tax - If its average rate increases as income increases. Such a tax claims not only a larger absolute (dollar) amount but also a larger percentage of income as income increases.

Personal income tax

Regressive tax - If its average rate declines as income increases. Such a tax takes a smaller proportion of income as income increases. A regressive tax may or may not take a larger absolute amount of income as income increases.

Sales tax

Payroll taxes

Property taxes

Proportional tax - If its average rate remains the same regardless of the size of income

Corporate income tax

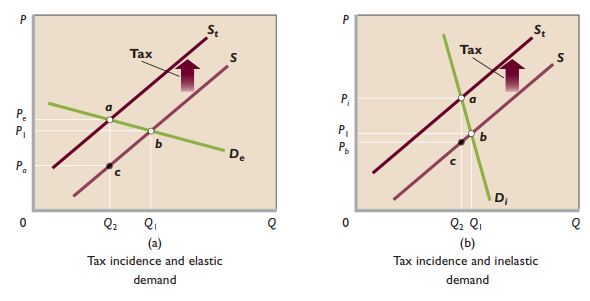

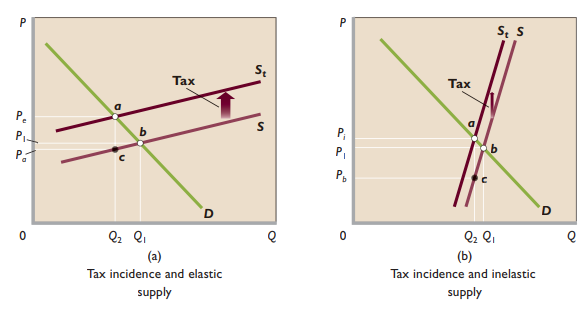

Tax incidence - Final resting place of a tax (who pays it?)

More inelastic demand → Larger portion of tax shifted to consumers

More inelastic supply → Larger portion of tax shifted to producers

Efficiency loss of the tax - This loss is society’s sacrifice of net benefit, because the tax reduces production and consumption of the product below their levels of economic efficiency, where marginal benefit and marginal cost are equal

Demand more elastic → Efficiency loss greater

Probable incidence of US taxes

Incidence of personal income tax is on individual

Incidence of corporate income tax is on company’s stockholders

Incidence of property tax is on property owner

US tax structure

Federal tax system is progressive

State + local tax structures are largely regressive

Overall US tax system is slightly progressive