Ch 1 - What is Economics?

Economics: the study of the choices that people make in overcoming the problems that arise because resources are limited, while needs and wants are unlimited.

Scarcity: in a state of being in short supply

Opportunity cost: whenever a choice is made by an economic agent concerning the use of its resources, something is given up or sacrificed.

The next best alternative when an economic decision is made, a “trade-off”

If there is no scarcity if a good, and everyone can have as much as they want, it is called a free good

Example:

Air is a free good

Breathable air is an economic good

Economic good: is one that is scarce and whose use involves an opportunity cost

Sustainability: ability to be maintained at a certain rate or level

Microeconomics: the choices consumers and producers make in response to the changes in the dynamic world

a. Examines how producers and firms make decisions to improve efficiency

b. Examines how producers and firms make decisions to improve efficiency

c. considers individual industries to see how producers interact with each other and how government intervention may affect producers

Macroeconomics: focuses on the factors affecting the economy as a whole, such as economic growth and the way well being is being maintained by economic growth.

a. Looks at the way income is distributed in an economy (inflation, deflation, unemployment).

Why does the government intervene in markets and in economies?

In terms of microeconomics:

a. To make sure the products meet a certain standard

b. To encourage sustainability

c. To prevent large firms from abusing their ability to influence markets

In terms of macroeconomics:

a. To encourage businesses to produce more to increase gross national income

b. To encourage businesses to produce more to increase gross national income

c. Reduce levels of unemployment

d. Improve economic well-being of workers

9 central concepts of Economics:

Scarcity: limited amount of resources in the economy

Choice: measures opportunity cost, determines the choice of selecting alternative options in regards to scarcity of goods or services.

Equity: distributing wealth in the economy fairly, unlike equally

Sustainability: preserving current resources in order to ensure that future generations and economies thrive off of the resources

Intervention: As in government intervention, when it takes over and gets involved to help economies

Change: constant state of change in an evolving economy

Economic well-being: general well being of the economy to ensure that societies can prosper from its resources

Interdependence: extent to which economies and countries rely on each other

Efficiency: achieving economic progress using as little resources as possible in order not to drain the economy

Tip: These central key concepts are to be used in the IA, and are the main focal point of the Economics syllabus, understand them well

Four factors of production:

Land: includes all the resources provided by nature that are used to produce goods. Also known as “natural capital”

Labour: includes all the human resources used in producing goods. Also known as “human capital”

Capital: includes buildings, offices, factories, machines, tools, infrastructure and tech to produce goods and services. Also known as “physical capital”

Entrepreneurship (management): organising and risk taking factor of production. Entrepreneurship organise land, labour, and capital to produce goods and services

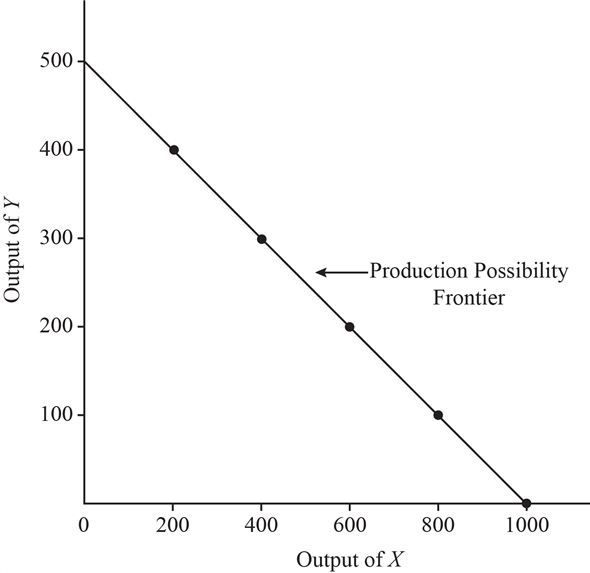

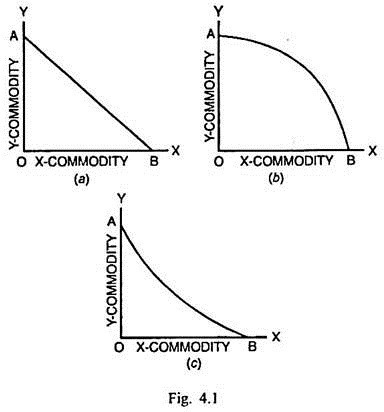

Production possibilities curve (PPC): Is a curve that represents all possible combinations of goods/services in a country using the available resources. Represented by a simple model which conveys two goods or services at any given time

Opportunity cost

Choices

Allocation of resources

Due to scarcity, the economy cannot produce enough agricultural goods due to the lack of resources. All the points beyond the PPC curve are unattainable given the current resources and state of technology

A choice has to be made between the outputs competing for the economy’s resources. A choice have to be made as to which combination of output is to be produced using which resources

Productive efficiency: when the economy is using all of its resources to the fullest extent possible

Lack of efficiency: waste of resources

Actual economic growth: any movement which indicates that more output is being produced

A straight line PPC indicates constant opportunity costs

A concave PPC indicates increasing opportunity costs

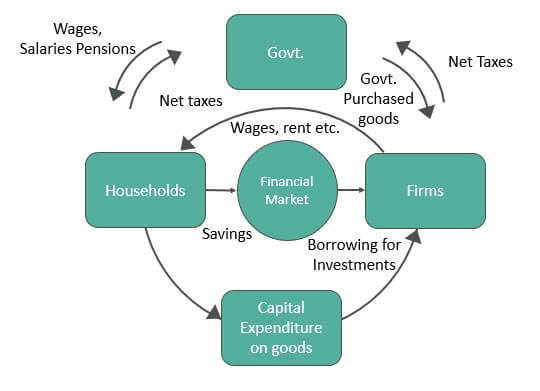

Circulation of money in the economy:

Leakage: any income that leaves the firm sector

The three leakages:

Taxes: some income from firms and households goes to the government sector in the form of taxes

Savings household and firm sector save some of their income in financial institutions (such as: banks, stock markets, pension funds) → these make up the financial sector

Imports: household and firm sectors spend money on foreign goods and services

Gross national income (GNI): amount of money in circular flow

When GNI is rising, the economy is expanding. When GNI is falling, the economy is in recession.

Planned Economy: decisions as to what to produce, how to produce, and for whom, are made by the government

Sometimes called a centrally planned economy or command economy

The government arranges all production, set wages, and set wages

Free market economy: all production is in private hands and demand and supply are left free to set wages and prices in the economy

Few cases of shortage → efficient work

Called private enterprise economy or capitalism

Prices are used to ration goods and services