Chapter 3 - Exchange and Markets

3.1 Comparative Advantage and Exchange

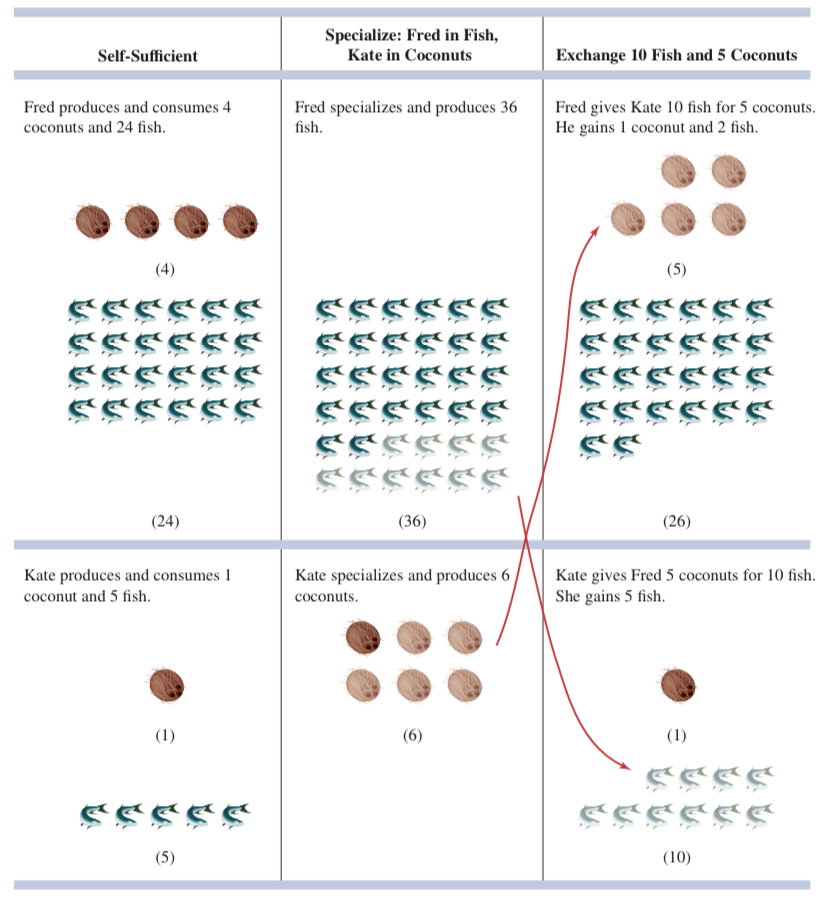

A market is an institution or arrangement that enables people to buy and sell things. An alternative to buying and selling markets is to be self-sufficient, with each of us producing everything we need for ourselves.

Rather than going it alone, most of us specialize: We produce one or two products for others and then exchange the money we earn for the products we want to consume.

Specialization and the Gains from Trade

Two survivors will be better off if each person specializes in one product and theme exchanges with the other person.

Principle of Opportunity Cost: The opportunity cost of something is what you sacrifice to get it.

Specialization will increase the total output of our little survivor economy.

We say that a person has a comparative advantage in producing a particular product if he or she has a lower opportunity cost than another person.

If specialization is followed by change, both people will be better off.

Principle of Voluntary Exchange: a voluntary exchange between two people makes both people better off.

Comparative Advantage versus Absolute Advantage

Absolute Advantage: The ability of one person or nation to produce a product at a lower resource cost than another person or nation.

The Division of Labor and Exchange

Adam Smith noted that specialization actually increased productivity through the division of labor.

He listed 3 reasons for productivity to increase with specialization, with each worker performing a single production task:

Repetition: The more times a worker performs a particular task, the more proficient the worker becomes at that task

Continuity: A specialized worker doesn’t spend time switching from one task to another.

Innovation: A specialized worker gains insights into a particular task that leads to better production methods.

Specialization and exchange result from differences in productivity that lead to comparative advantage.

Differences in productivity result from differences in innate skills and the beliefs associated with the division of labor.

Comparative Advantage and International Trade

Comparative advantage and specialization apply to trade between nations. Each nation could be self-sufficient, producing all the goods it consumes, or it could specialize in products for which it has a comparative advantage.

An import is a product produced in a foreign country and purchased by residents of the home country.

An export is a product produced in the home country and sold in another country.

Outsourcing

When a domestic firm shifts part of its production to a different country, we say the firm is outsourcing or offshoring.

Firms shift functions such as customer service, telemarketing, document management, and medical transcription overseas to reduce production costs, allowing them to sell their products at lower prices.

Studies of outsourcing found conclusions:

The loss of domestic jobs resulting from outsourcing is a normal part of a healthy economy because technology and consumer preferences change over time.

The jobs lost to outsourcing are at least partly offset by jobs gained through insourcing, jobs that are shifted from overseas to the United States.

The cost savings from outsourcing are substantial, leading to lower prices for consumers and more output for firms.

3.2 Markets

In a market economy, most people specialize in one productive activity by picking an occupation and using their incomes to buy most of the goods they consume. In addition to the labor and consumer markets, many of us participate in the market for financial capital.

Social and government inventions have made markets work better:

Contracts specify the terms of exchange, facilitating exchange between strangers.

Insurance reduces the risk entrepreneurs face.

Patents increase the profitability of inventions, encouraging firms to develop new products and production processes.

Accounting rules provide potential investors with reliable information about the financial performance of a firm.

Virtues of Markets

Centrally Planned Economy: An economy in which the government bureaucracy decides how much of each good to produce, how to produce the good, and who gets the good.

In order to make these decisions, a planner must first collect a huge amount of widely dispersed information about consumption desires (what products each individual wants), production techniques (what resources are required to produce each product), and the availability of factors of production (labor, human capital, physical capital, and natural resources).

Then, the planner must decide how to allocate the productive resources among the alternative products.

Finally, the planner must divide the output among the economy’s citizens.

Under a market system, decisions are guided by prices of inputs and outputs and made by the millions of people who already have information about consumers’ desires, production technology, and resources.

In a market system, prices provide individuals with the information they need to make decisions.

Prices provide signals about the relative scarcity of a product and help an economy respond to scarcity.

The decisions made in markets result from the interactions of millions of people, each motivated by his or her own interest.

The market system works by getting each person, motivated by self-interest, to produce products for other people.

The Role of Entrepreneurs

Prices and profits provide signals to entrepreneurs about what to produce.

Entrepreneurs will enter the market and increase production to meet the higher demand, switching resources from the production of other products. As entrepreneurs enter the market, they compete for customers, driving the price back down to the level that generates just enough profit for them to remain in business.

Entrepreneurs will leave the unprofitable market, finding other products to produce, and the price will eventually rise back to the level where profits are high enough for the remaining producers to justify staying in business.

3.3 Market Failure and the Role of Government

Market failure happens when a market doesn’t generate the most efficient outcome.

Reasons for Market Failure:

Pollution

Public goods

Imperfect information

Imperfect competition

The government enforces property rights by protecting the property and possessions of individuals and firms from theft.

The protection of private property guarantees that people will keep the fruits of their labor, encouraging production and exchange.

Roles of government:

Establishing rules for market exchange and using its police power to enforce the rules

Reducing economic uncertainty and providing for people who have lost a job, have poor health, or experience other unforeseen difficulties and accidents.

Government Enforces the Rules of Exchange

The market system is based on exchanges between strangers. These exchanges are covered by implicit and explicit contracts that establish the terms of trade.

To facilitate exchange, the government helps to enforce contracts by maintaining a legal system that punishes people who violate them. This system allows people to trade with the confidence that the terms of the contracts they enter will be met.

In the case of consumer goods, the implicit contract is that the product is safe to use. If a consumer is harmed by using a particular product, the consumer can file a lawsuit against the manufacturer and seek compensation.

The government also disseminates information about consumer products. The government requires firms to provide information about the features of their products, including warnings about potentially harmful uses of the product.

The government uses antitrust policy to foster competition by

Breaking up monopolies

Preventing firms from colluding to fix prices

Preventing firms that produce competing products from merging into a single firm

Government Can Reduce Economic Uncertainty

Given the uncertainty of market economies, most governments fund a “social safety net: that provides for citizens who fare poorly in markets.

The safety net includes programs that redistribute income from rich to poor, from the employed to the unemployed

A safety net is created to guarantee a minimum income to people who suffer from job losses, poor health, or bad luck.

Private insurance works when enough low-risk people purchase insurance to cover the costs of reimbursing the high-risk people.

As a result of insurances being unavailable to the private insurance markets, the government steps in to fill the void.