cash flow from operating activities

working capital = current asset - current liabilities

indicator of company's ability to generate sustainable cash flows through operations and management of working capital

focus on income statement and changes in current assets and liabilities from balance sheet

Cash inflows for operating activities

sale of goods or services

collection of interest and dividends

cash outflows for operating activities

purchase of inventory

payment for operating expenses

payment of interest

payment of income taxes

cash flow from investing activities

focus on changes in PPE, long term investments and assets from balance sheet(depreciation, gains/losses on sale of PPE and other LT assets)

cash inflow for investing activities

sale of debt/equity investments

sale of PPE

Collection of loan/notes receivable

cash outflow for investing activities

purchase of PPE

purchase of debt or equity

loans to other corporations

cash flows from financing activities

focus on long-term debt and stockholder's equity from balance sheet

cash inflows for financing activities

issuance of bonds or notes payable

issuance of stock

reissuance of treasury stock

cash outflows for financing activities

repayment of bonds or notes payable

acquisition of treasury stock

payment of dividends

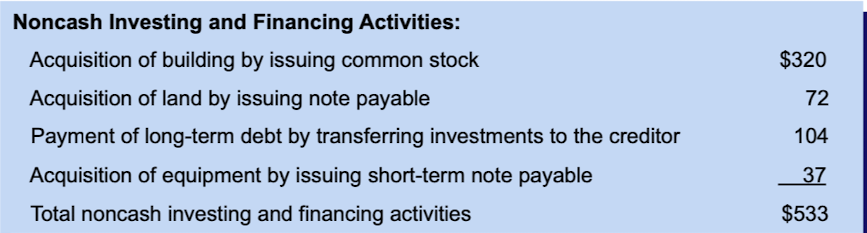

noncash activities

-significant investing and financing activities that do not affect cash -reported after the cash flow statement or in a note to the financial statements Examples

purchase long term assets by issuing debt

indirect method (operating activities)

begin with net income

list adjustments to net income to arrive at operating cash flows

direct method (operating activities)

adjust the items in the income statement to directly show the cash inflows and outflows from operations

operating activities (indirect method adjustments)

Non cash items (depreciation expense)

Non operating items (gains and losses on sale of assets)

changes in current assets and current liabilities (increase in account receivables is the amount of revenue reported in the income statement but not yet collected in cash)

indirect method (adjustment for non-cash activities included in net income)

amortization expense +depreciation expense

indirect method (adjustment for non-operating activities included in net income)

loss on sale of assets

gain on sale of assets

indirect method (adjustment for non cash part of operating activities included in net income)

increase in a current asset +decrease in a current asset -increase in a current liability +decrease in a current liability

direct method (cash received from customers)

net sales-increase in accounts receivable=cash received from customers

direct method (cash paid to suppliers)

cost of goods sold - decrease in inventory = purchases purchases + decrease in accounts payable = cash paid to suppliers

direct method (cash paid for operating expenses)

operating expenses + increase in prepaid rent = cash paid for operating expenses

direct method (cash paid for interest expense)

interest expense - increase in interest payable = cash paid for interest

direct method (cash paid for income taxes)

income tax expense + decrease in income tax payable = cash paid for income taxes

cash flow from operating activities

+sale of long-term assets -purchases of long term assets +collections of notes receivables -loans to others

cash flows from financing activities

issuance of shares

purchases of treasury shares

sale of treasury stock +issuance of notes and bonds payable (face value) -payment of notes and bonds payable -payment of dividens

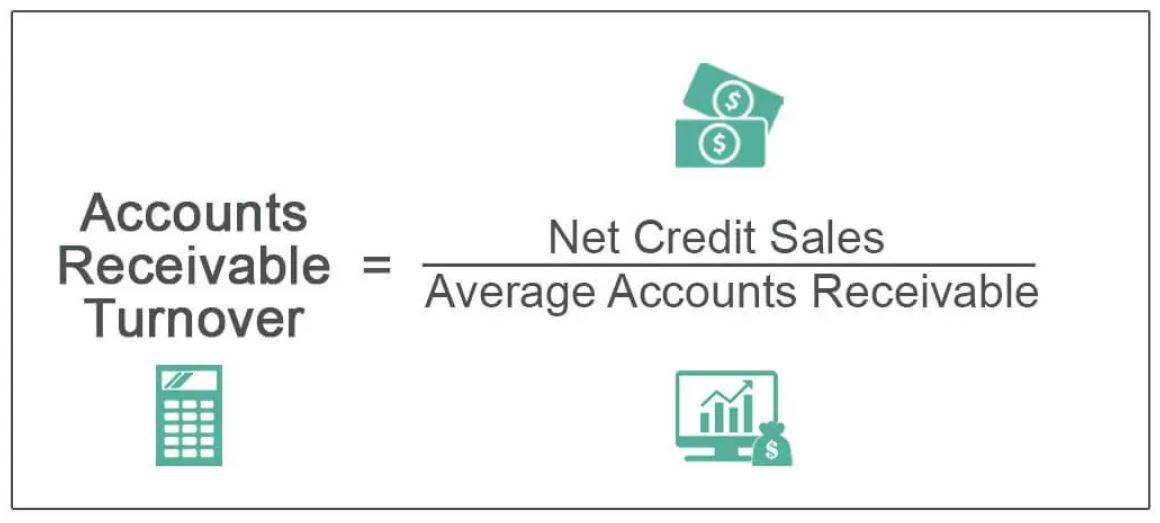

receivables turnover ratio (risk ratio)

measures how many times receivables are collected during year higher ratio indicates ability to quickly turn receivables into cash low ratio indicates trouble collecting receivables

average collection period(risk ratio)

measures the days it takes to convert receivables into cash shorter period maximize the speed of cash inflow AVP= 365/receivables turnover ratio

inventory turnover ratio(risk ratio)

measures how many times average inventory is sold during the year ITR= cost of goods sold/average inventory

Average days in inventory(risk ratio)

measures the average number of days it takes to sell its entire inventory during the year ADI=365/inventory turnover ratio

current ratio(risk ratio)

compares current asset to current liabilities A high current ratio indicates sufficient assets to cover its current obligations CA= current assets/current liabilities

Acid-test ratio(risk ratio)

more conservative measure of a company's ability to pay current liabilities ATR= (cash+current investments+A/R)/current liabilities

Debt to Equity Ratio(risk ratio)

indicates the risk of bankruptcy DtoER=Total liabilities/stockholder's equity

times interest earned ratio(risk ratio)

compares interest payments with income available to pay them measure of solvency TIER=(net income + interest expense +tax expense)/interest expense

gross profit ratio (profit ratio)

indicates the portion of each dollar of sales above its cost of goods sold GPR=gross profit/net sales gross profit = net sales - cost of goods sold

return on assets (profit ratio)

measures the income the company earns on each dollar invested in assets ROA=net income/average total assets

net income/average total assets=(net income/net sales)*(net sales/average total assets)

profit margin (profit ratio)

measures the income earned on each dollar of sales PM=net income/net sales

asset turnover (profit ratio)

measures sales volume in relation to the investment in assets AT = net sales / average total assets

return on equity (profit ratio)

measures the income earned for each dollar in stockholders' equity ROE= net income/average stockholders' equity

earnings per share (profit ratio)

EPS= (net income - dividends on preferred stock)/(average shares of common stock outstanding)

price-earnings ratio (profit ratio)

compares a company's share price with its earnings per share PER= stock price/earnings per share

balance sheet

Asset= liabilities + equity assets = liabilities + (stockholder's equity + (revenue-expenses)-dividends) net assets = assets - liabilities

income statement

Net income = revenues - expenses

statement of stockholder's equity

ending retained earnings = beginning retained earnings + net income - dividends stockholder's equity = common stock/ share capital + retained earnings

matching principle

Revenue of the period is matched with expenses required to create those revenues

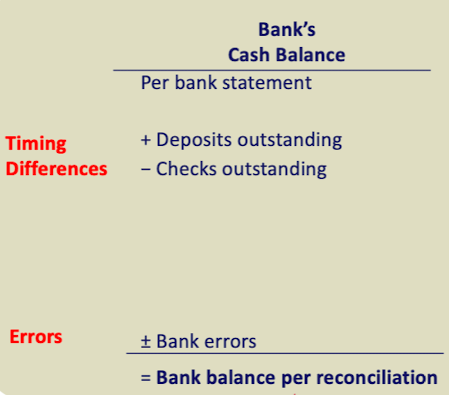

Bank's cash balance (bank reconciliation)

per bank balance +deposit outstanding -checks outstanding +/- banks errors

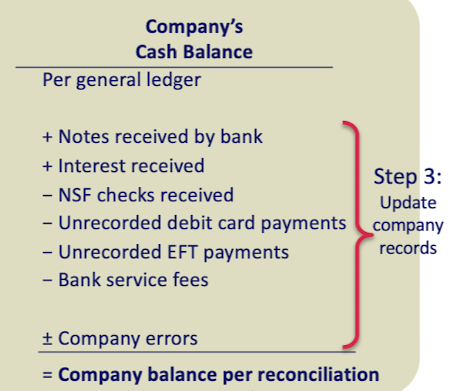

company's cash balance (bank reconciliation)

per general ledger +notes received by bank +interest received -NSF checks received -unrecorded debit card payments -unrecorded EFT payments -bank service fees +/- company errors

net sales

sales revenue (including trade discounts)-sales returns and allowances - sales discounts = net sales

FOB shipping point

-buyer pays for the freight charge -freight is part of inventory cost -buyer records it when the goods leave the supplier -seller records it when the goods leave the seller

FOB shipping destination

freight charge is paid by the seller

freight charges become part of cost of goods sold -buyer records it when they receive the goods -seller records it when the buyer receive the goods

inventory purchases

purchase price + freight in - purchase returns - purchase allowances - purchase discounts = net purchases

freight in

transportation cost paid by the buyer under FOB shipping point

Inventory sales

sales revenue - sales returns and allowances - sales discounts = net sales

weighted average cost

average cost per unit = cost of goods available/number of units available goods available = beginning inventory + purchases